Cigarette makers argue they should be considered an ESG stock because of attempts to shift towards healthier alternatives. What does it say about sustainable investing?

- Jamie Dimon referred to JPMorgan’s former general counsel as the “ultimate decider” on whether to drop Jeffrey Epstein as a client.

- Amazon will pay $31 million to settle allegations it violated the privacy of customers through its Alexa and Ring doorbell products.

- UK house prices fell at their fastest pace in 14 years (more below).

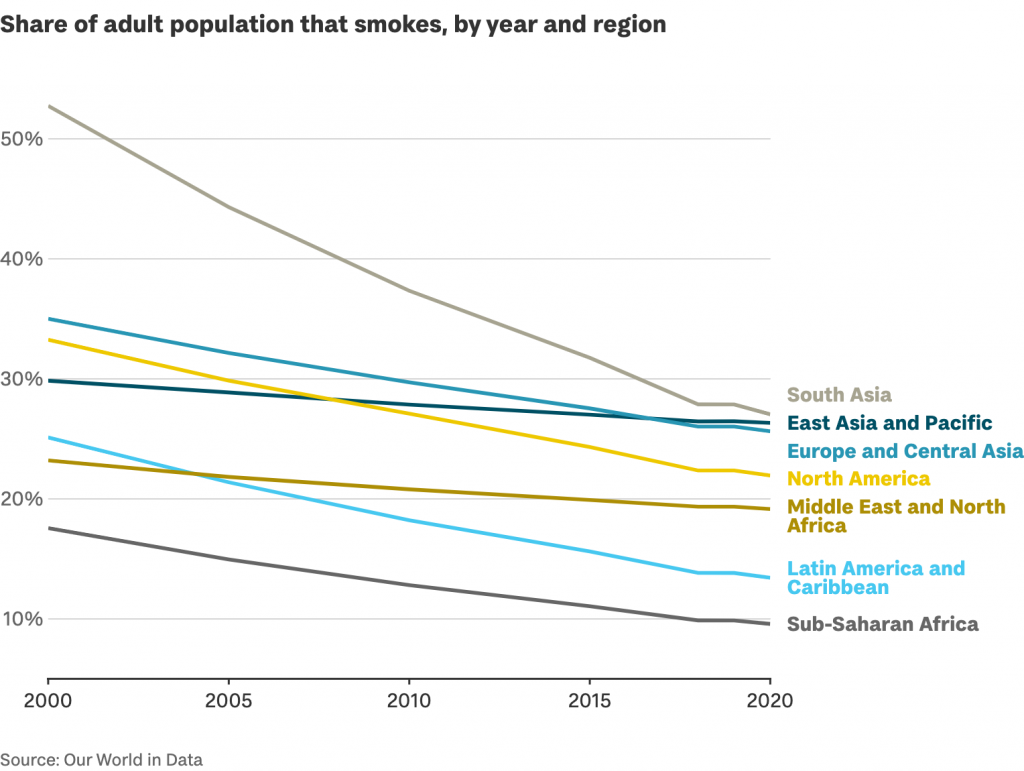

Most fund managers quit smoking long ago. Big Tobacco has a plan to change that.

Jacek Olczak, CEO of Philip Morris International, maker of Marlboros, claimed his company is on a path to becoming an ESG stock as it shifts away from cigarettes to vapes. British American Tobacco, under its new CEO Tadeu Marroco, is equally focused on a drive to be seen as sustainable, again by moving to non-combustible nicotine.

So what? Tobacco stocks will never be an ESG-friendly pick. The industry’s history of harming consumers and deceiving society is too pungent for that.

But the cigarette-makers’ eagerness to be admitted to the world of ‘good business’ reveals something telling about the limits of ESG and the contrasting roles of government, the board and the courts.

By the numbers:

62 – percentage share of global equity funds that avoid tobacco entirely, according to a Russell Investments study.

$6 billion – value of discounts paid by manufacturers to cigarette retailers in the US in 2021, to reduce the price for consumers.

15 – percentage share of early deaths worldwide attributable to smoking.

Tobacco companies – along with other sin industries – have high profit margins, strong cash flow and scope for substantial cash returns to shareholders, as Russ Mould, an investment director at AJ Bell points out.

Take them at their word, and the industry could become a valuable element of an ESG portfolio if it could deliver across key metrics such as carbon emissions, labour rights and good governance.

But that highlights a weakness of the ESG approach. The definition of a sustainable business may not be broad enough to encompass the true scale of the risk.

Tech stocks tend to be ESG darlings: Microsoft, Alphabet, Apple and Visa all usually feature in sustainable funds. Writing code tends to have lower emissions and less fraught supply chains than bashing metal.

But, as the leaders of Open AI admitted last week, what’s at stake can be hard to capture in existing measures: AI systems carry with them the prospect of “existential risk” to humanity.

There’s a gap between what ESG can govern and what falls to the law to govern.

Ultimately, limiting socially destructive side-effects of business will require one of two things: regulators willing to bare their teeth, or a board directors’ equivalent of the Hippocratic Oath.

A final, related thought: this week members of the Sackler family were granted immunity from civil claims relating to Purdue Pharma, makers of Oxycontin. They agreed in return to make payments of up to $6bn for survivors, victims and families. The same day, Elizabeth Holmes began her prison sentence for a fraud whose victims were wealthy investors and companies.

Looking at these contrasting outcomes prompts the question: how does corporate justice work?